🚨Industry Perspective: Board Member Spotlight Blog #2

We’re excited to feature Ethan Arbiser, newly appointed REEF Board Member and Senior Manager of Energy & Sustainability at CBRE. Ethan has led sustainability strategies across global real estate portfolios for companies including Intuit and The Cigna Group—advancing initiatives in energy, water, waste, and net-zero planning. With deep expertise in carbon reduction, renewable energy, and ESG reporting, Ethan brings a critical vantage point on refrigerants as both a climate risk and a strategic asset issue for the built environment.

Stay tuned as we dive into his perspective on how commercial buildings, ESG drivers, and procurement decisions can shape the future of refrigerant management and recovery.

🏢 The Built Environment as a Refrigerant Policy Driver

Q: From your work across major real estate portfolios, what are the biggest operational or financial barriers preventing building owners from proactively managing refrigerants, and how do you see refrigerants fitting into broader ESG and net-zero planning moving forward?

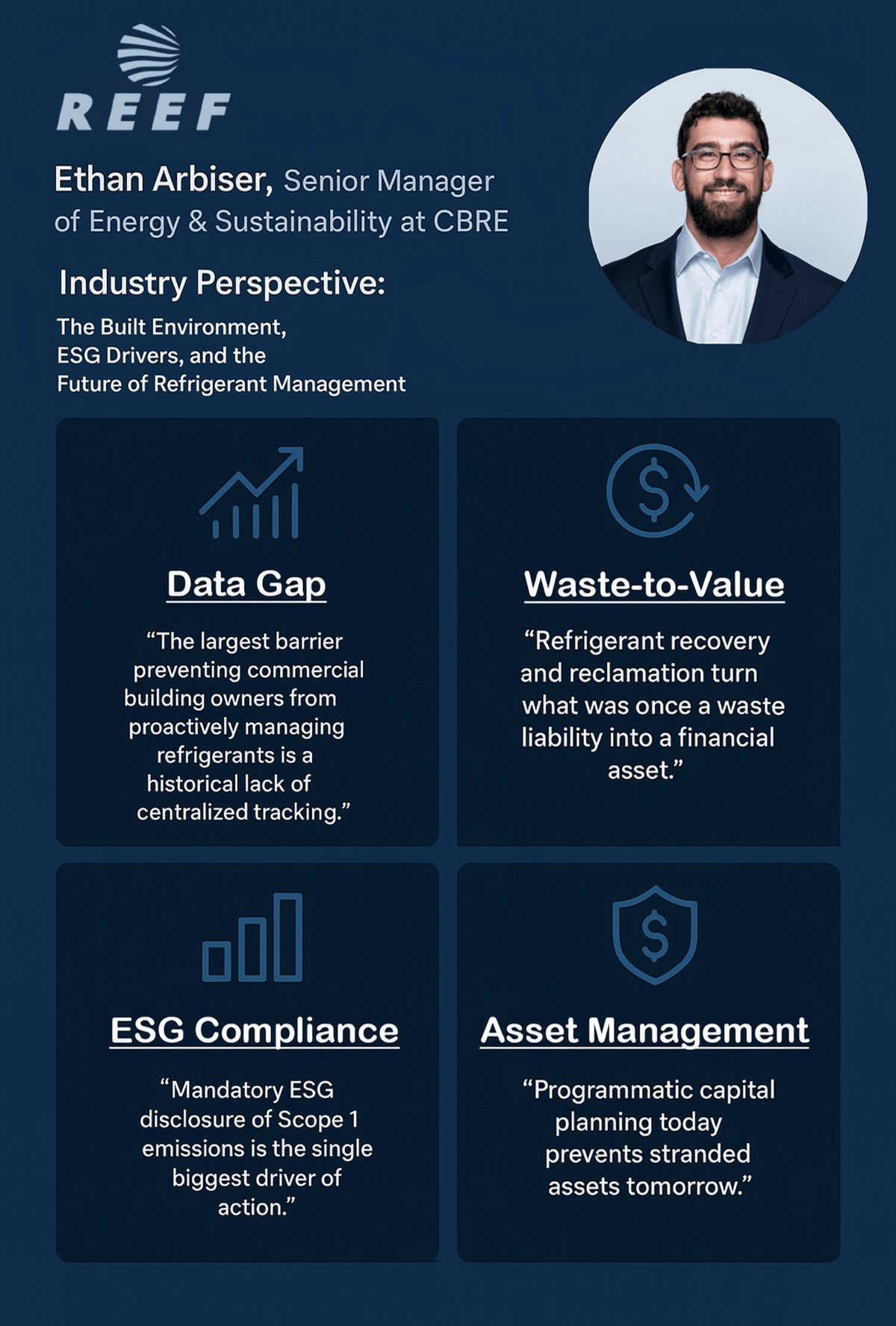

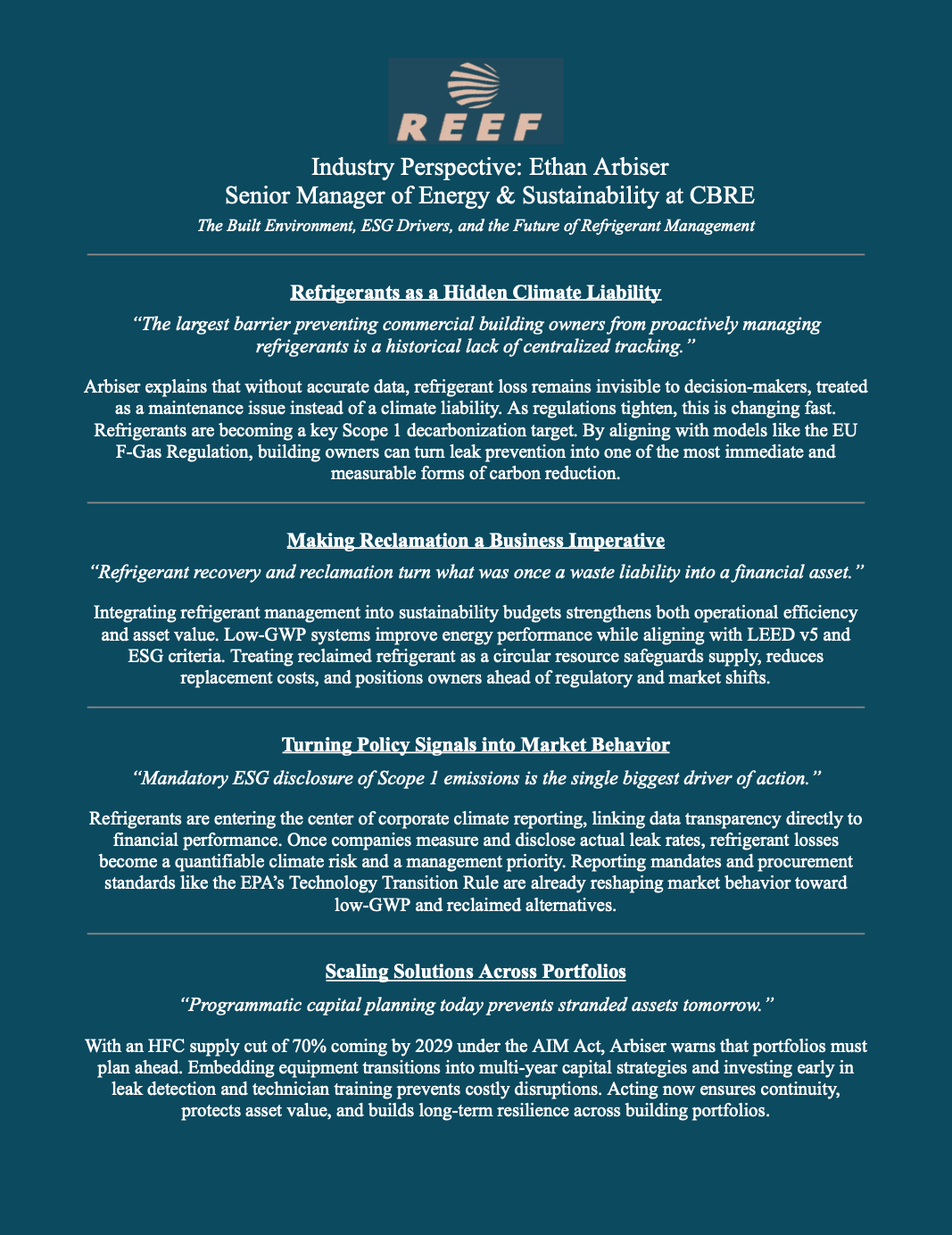

A: The largest barrier preventing commercial building owners from proactively managing refrigerants is a historical lack of centralized tracking, leading to reliance on estimates rather than actual usage and leak data. Without this granular data, refrigerant loss is treated merely as a maintenance cost, rather than a significant climate liability that demands executive attention and capital planning. However, the regulatory environment is rapidly forcing a change, positioning refrigerants—which primarily contribute to Scope 1 (direct) emissions as fugitive gases—at the core of ESG and Net-Zero planning. A single major leak of a high-GWP refrigerant can equate to thousands of tons of C02e, possibly negating an entire years’ worth of energy efficiency progress. It can be argued that leak mitigation is the single most powerful lever for immediate Scope 1 decarbonization. The EU F-Gas Regulation, with its declining quotas and specific equipment bans, serves as a strong model for policy, mandating a market shift toward lower-GWP alternatives.

♻️ Making Reclamation + Recovery a Business Case

Q: Real estate owners already track energy, water, and waste. What would it take for refrigerant and reclaimed gas procurement to become a standard line item in sustainability budgets, alongside efficiency or renewables?

A: The most compelling business case for integrating refrigerant management into sustainability budgets centers on operational efficiency and asset protection. When facility teams adopt low-GWP refrigerants, they are often required to install newer, highly efficient HV AC systems that are engineered for smaller charge sizes and lower leak rates. This advanced equipment improves a building’s energy performance,which translates directly into reduced energy expenses over the asset’s lifetime, helping to offset the initial capital investment. Furthermore, implementing best practices for refrigerant recovery and reclamation—as encouraged by guidelines like LEED v5—extends the life of valuable resources, turning what was once a waste liability into a financial asset, especially as the supply of virgin high-GWP refrigerants shrinks under phase-down rules.

📊 Turning Policy Signals into Market Behavior

Q: You’ve seen how incentives, reporting, and disclosure drive action in buildings. Which policy tools (rebates, mandates, procurement standards, ESG reporting, leasing requirements) would most effectively push commercial property owners to adopt reclaimed refrigerants and low-GWP alternatives?

A: Policy tools most effectively push commercial property owners toward reclaimed and low-GWP refrigerants by elevating the issue through mandatory reporting, forcing data scrutiny. The biggest single driver is mandatory ESG disclosure of Scope 1 fugitive emissions, which directly ties a building’s climate impact to corporate financial reporting. This required transparency is compelling the industry to transition from relying on estimates for refrigerant loss to gathering and verifying actual operational data on leak rates and service charges, achieving a level of rigorous data accountability similar to that already established for energy and water consumption. This operational data, now at center stage, demonstrates the material risk of high-GWP assets, making their transition unavoidable. This market behavior is then locked in place by mandates and procurement standards, such as the U.S. EPA’s Technology Transition Rule, which restricts or bans the use of high-GWP refrigerants in all new equipment.

🔑 Scaling Solutions Across Portfolios (Not Just Pilots)

Q: With refrigerant shortages expected by 2029, how can large portfolios prepare now, through capital planning, equipment transition timelines, or supplier engagement, to avoid cost shocks and stranded assets?

A: To effectively prepare for refrigerant shortages—particularly the 70% reduction in HFC production/imports scheduled for 2029 under the AIM Act—large portfolios must shift to programmatic capital planning. This involves proactively integrating the transition to low- GWP equipment into 3-5 year capital expenditure plans, and possibly even longer. This strategy allows owners to manage the cost of replacement and avoid emergency, costly retrofits when old systems fail. Furthermore, early engagement with suppliers and technology providers is crucial to secure the future supply of low-GWP refrigerants and equipment. This must be supported by significant investment in workforce education and the installation of automatic leak detection systems (ALDS), which reduce immediate losses and protect both the assets and the environment.